Money

Why Your Auto Insurance Coverage Is the Biggest Risk to Your Net Worth

Zach Rodriguez|June 9, 2026|Read time: 8-10 minutes

Personal injury law is a $61.7B industry. Learn why your auto liability limits may be exposing your net worth.

On a Saturday night last fall, I was reviewing a client's property and casualty insurance policies. Riveting, right?

These clients were a couple in their early thirties living in California with a combined income north of $400,000 per year, owned multiple rental units and had a net worth over $2.5 million. In fact, they had one of the more sophisticated estate planning structures I've seen for a thirty something couple; a revocable living trust, multiple LLCs held under a Nevada holding company. By almost every measure, their estate plan (and financial life) was rock solid.

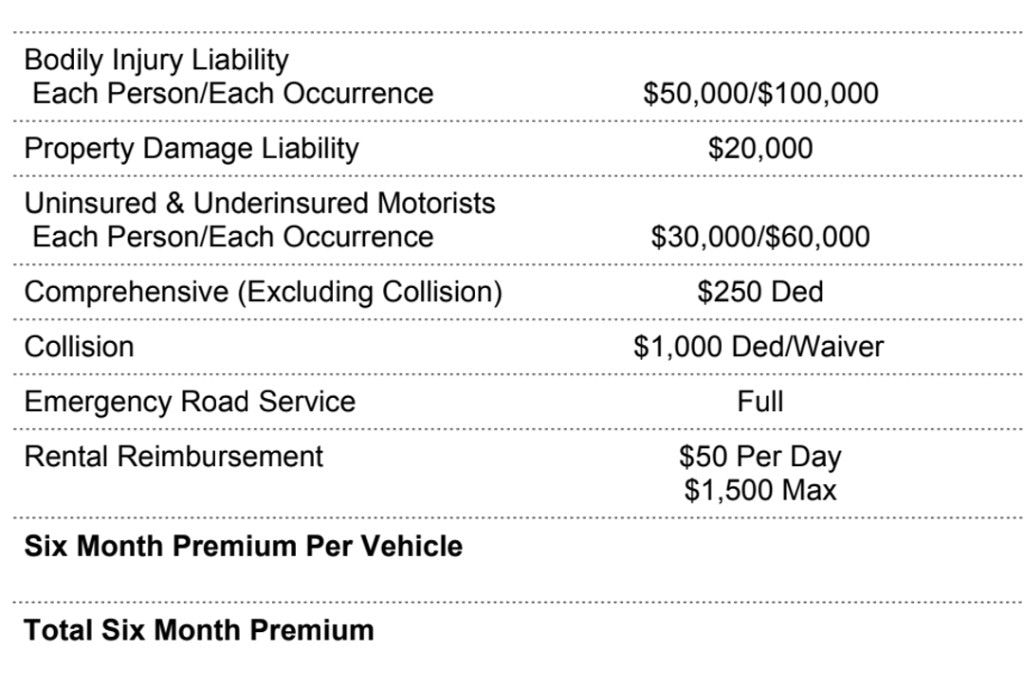

Then I looked at their auto policy and immediately stress-texted them… I've included it below so you can take a look. See any issues?

Before we get into it, a quick note on scope. This article focuses specifically on the liability side of your auto policy. Not collision or comprehensive.

Underinsurance is a Net Worth Problem, Not Just an Insurance Problem

Most people think of auto insurance as a product you buy to fix your car if you are involved in an at-fault accident. While it does serve that purpose, there is another. For anyone with meaningful assets, auto insurance is also a liability protection tool.

Have you ever noticed the plethora of personal injury law firm billboards that litter the highway on your commute? Of course you have. Personal injury law is one of the most lucrative legal markets in the United States. The industry generated $61.7 billion in revenue in 2025, according to IBISWorld. These firms operate almost exclusively on contingency, meaning they take a percentage of whatever they win for their client, typically 33% to 40%.

Here is what happens if you cause a serious accident and injure someone:

- The injured party files a lawsuit against you personally.

- Their attorney assesses the damages including medical bills, lost wages, pain and suffering, and long-term care costs, then pursues a judgment.

- Your insurance company pays up to your policy limit.

- The court issues a judgment for the remaining balance. That balance is now your personal liability.

- To collect, the plaintiff can go after your brokerage account, your home equity, and your future wages through garnishment.

- Depending on your state, even certain retirement accounts may not be fully protected. For example, California offers more limited creditor protection for IRAs than states like Texas or Florida.

What do the first three numbers on your auto policy mean?

First, it helps to understand when these numbers matter. When you are involved in an accident, there are generally three scenarios:

- You are not at fault. The other driver's insurance is responsible for your damages.

- The other driver is uninsured or underinsured. We will cover that in its own section shortly.

- You are at fault. This is where your policy limits become critical.

One caveat worth noting: some states operate under no-fault insurance laws, meaning each driver's own insurance covers medical bills regardless of who caused the accident. In those states, the dynamic is different.

The first number: Bodily injury per person. This is the maximum your insurance will pay to a single injured person in an accident you cause. According to USAA, "This helps cover expenses for the injuries or deaths of others involved in accidents where you're found at fault. This can include the other driver's medical expenses, pain and suffering, and your legal defenses if you're sued."

The second number: Bodily injury per accident. This is the total your policy pays out across all injured parties in a single accident, regardless of how many people are hurt. Using my client's policy as an example, that was $100,000. If they were to hit a vehicle with two seriously injured people, that $100,000 gets divided between them. And medical bills beyond the $100,000 would have been their responsibility.

The third number: Property damage per accident. This is the maximum your policy will pay to repair or replace someone else's vehicle or property when you are at fault. According to Kelley Blue Book, the average transaction price for a new vehicle in the United States surpassed $50,000 for the first time in 2025. Total a newer truck or SUV and you are writing a personal check for the difference.

The Coverage Gap That Gets Overlooked: Uninsured and Underinsured Motorist

Uninsured and underinsured motorist coverage or UM/UIM protects you when someone else causes an accident and either has no insurance or doesn't have enough to cover your damages. More than one in seven drivers on the road today are uninsured. In some states, that number is closer to one in four.

If an uninsured driver runs a red light and puts you in the hospital, your own UM coverage is what pays your medical bills, your lost income, and your recovery costs. Without adequate UM/UIM limits, you're absorbing those costs yourself or chasing a defendant who has nothing. State Farm recommends choosing UM/UIM limits that match your bodily injury liability limits, noting it provides equal protection whether you are at fault or someone else is.

How to Think About the Right Coverage Level

Your auto liability coverage should increase as your net worth does, and your bodily injury limits should reflect the assets you stand to lose if a judgment is brought against you.

Consumer Reports recommends 100/300/100 as a good baseline for most drivers, and steps that up to 250/500/250 for anyone with significant financial assets, noting it helps prevent creditors from coming after savings and home equity.

For context, 250/500 bodily injury limits mean your insurer covers up to $250,000 per person and $500,000 per accident. For my client with a $2.5 million net worth, this leaves significant personal assets exposed in a worst-case scenario. That gap is where a personal umbrella policy comes in.

Think of an umbrella as an additional financial backstop that sits above your auto and homeowners' policies and kicks in when an underlying limit is exhausted. A $1 million umbrella policy runs roughly $383 per year, with each additional million adding around $75 annually.

Action Steps

- Review your auto declarations page and locate the numbers in the picture above

- Shop your rates. Get competing quotes before making any changes. Most people are overpaying

- Raise your bodily injury limits to at least 100/300

- Consider bundling auto, homeowners, and umbrella with the same carrier to reduce the total cost

- Re-shop and review annually to make sure your coverage keeps pace with your net worth.

Conclusion: Focus on the Fundies

There is a tendency in personal finance, especially among high earners, to skip ahead to the 'advanced tactics.' Things like Roth conversions, alternative investments, or direct indexing, or a myriad of topics. Before that, start with the basics: An estate plan for your family, adequate life insurance, homeowners' coverage that reflects what your home is worth, a savings rate that moves the needle, and auto insurance limits that protect your net worth.

My client had the advanced stuff covered with a living trust, multiple LLCs, and a holding company. But a single at-fault accident on a California freeway could have unraveled years of careful planning because their coverage was too low.

First, get the fundies right. Then move on to the fun stuff!

Worried your auto coverage doesn't match your net worth?

Book a free intro call. We'll review your liability limits and how they fit your overall financial plan.