Tax Planning

Business Owners in High-Tax States Have a Tax Advantage Most Never Use

Zach Rodriguez|June 15, 2026|Read time: 6-8 minutes

Own a business in California, New York, or another high-tax state? PTET lets your business pay your state tax bill and deduct every dollar federally. Here is how it works.

What the Pass-Through Entity Tax election is, who qualifies, and how it works.

Most high earners in high-tax states know they are getting squeezed on their state tax bill. What most of them may not know is that if they own any part of a business, there is a legal, IRS-approved way to deduct their full state tax bill without hitting the federal cap. It is called the Pass-Through Entity Tax election, or PTET.

A Quick Word on SALT

For the purposes of this article, high earners are those in the 35% federal tax bracket or above, roughly $256,225 or more in taxable income for single filers and $512,450 or more for married couples filing jointly. At that income level in a high-tax state, your combined federal and state tax burden is significant enough that the SALT cap is almost certainly costing you money every year.

SALT stands for:

- State; state income taxes on your wages, business income, or investment gains

- And

- Local; local income or wage taxes charged by your city or county

- Taxes; property taxes on your home or other real estate

Before 2018, you could deduct every dollar of state and local taxes you paid from your federal return. Then the Tax Cuts and Jobs Act (TCJA) capped that deduction at $10,000. For high earners in states like California, New York, New Jersey, Hawaii, and Illinois, that cap effectively created a second tax on income that was already taxed by the state.

The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, raised that cap to $40,000 for 2025, increasing to $40,400 for 2026 with 1% annual increases through 2029. For 2026, the phaseout begins at $505,000 of Modified Adjusted Gross Income (MAGI). The $40,400 deduction is reduced by 30 cents for every dollar earned above that threshold, reaching the $10,000 floor at approximately $606,333 MAGI.

What Is PTET and How Does It Work

Here is the normal flow without PTET. Your business earns income. That income flows to your personal tax return. You owe state income taxes on it, but when you try to deduct those taxes on your federal return, you hit the $40,400 SALT cap. A portion of your state income taxes aren't deductible.

PTET changes where the tax gets paid. Instead of you paying state income taxes personally, your business pays them directly to the state. Because the business is paying the taxes, that tax is treated as a business expense on your federal return and not a personal deduction. Business expenses are not subject to the SALT cap.

The result: your full state tax bill on business income becomes a federal deduction. For single filers earning above $640,600 or married couples filing jointly earning above $768,700, the top federal marginal rate is 37%. At that rate, every $10,000 in state taxes your business pays on your behalf saves you $3,700 in federal taxes.

Who Qualifies and Is My State on the List

The simplest way to know if this applies to you: do you receive a K-1 at tax time?

A K-1 is the form that shows income flowing through to you from a partnership, S-corp, or multi-member LLC. If you get one, the entity behind it is exactly the type of structure that can make a PTET election. A lot of people who receive K-1s think of themselves as passive investors, silent partners, or part-time participants rather than business owners. For PTET purposes, that distinction does not matter. If income is passing through to you on a K-1, your entity likely qualifies.

In addition to a full-time business owner, this includes the co-founder of a small LLC, the partner at a professional services firm, the person with a stake in a real estate partnership, and the high earner running a side consulting practice structured as a multi-member LLC. It also includes someone who inherited a piece of a family business and collects a K-1 annually.

One important exception: single-member LLCs are generally not eligible unless they elect to be treated as an S-corp. Sole proprietors filing on Schedule C do not qualify either.

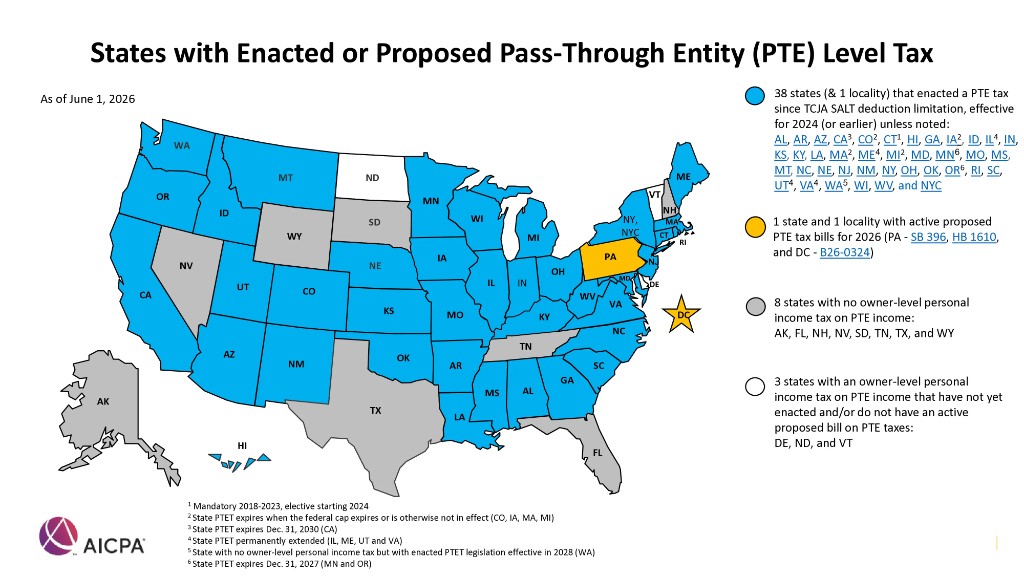

Approximately 36 states and New York City now offer a PTET election option. The map below, sourced from the Texas Society of CPAs and updated December 2025, shows which states currently have it. If you are in a no-income-tax state like Texas or Florida, PTET does not apply because there is no state income tax to shift.

A Tax Savings Example for a California Business Owner

Let's say you own a roofing company in California structured as an S-corp. The business generates $2,000,000 in revenue. After materials, labor, overhead, and paying yourself a $150,000 salary, $550,000 passes through to your personal return as business income. California taxes that at 13.3%, a state tax bill of roughly $73,150 on that income.

Without PTET, you can only deduct $40,400 (SALT Cap) of that $73,150 on your personal return. The remaining $32,750 is not recognized as a federal deduction. With PTET, your S-corp pays that $73,150 directly to California and deducts the full amount as a business expense, bypassing the SALT cap entirely. Your federal taxable income drops by $73,150. Multiply that by your 35% marginal federal rate and that is $25,602 back in your pocket thanks to the PTET election.

What You Need to Know Before You Elect

PTET is an annual election with no multi-year commitment. You can elect for 2026 and reassess for 2027 based on that year's income and tax picture. But once the election is made for a given year, it is irrevocable.

Deadlines are the most important thing to understand here, and every state that offers PTET has its own rules. They are not consistent. Some states require you to elect early in the year before your financials are even complete. Others allow you to elect up to the extended return due date. Missing the deadline in your state means losing the ability to elect PTET for that entire tax year with no exception. New York requires the election to be made between January 1 and March 15, with quarterly estimated payments due March 15, June 15, September 15, and December 15. New Jersey's election is made on the annual PTE-100 return by the original return due date of March 15. California requires a prepayment by June 15 equal to the greater of $1,000 or 50% of the prior year's PTET liability. Missing that prepayment no longer voids the election for 2026 and beyond, but it does reduce each owner's credit by 12.5% of their share of the underpaid amount. Because the rules vary so significantly from state to state, this is one conversation you need to have with your CPA before the window closes.

PTET and the expanded SALT cap are not mutually exclusive either. Even with the SALT cap raised to $40,400, it can still be beneficial for pass-through entities to elect PTET. For partnerships in a trade or business, deducting entity-paid PTET against business income also lowers the partners' shares of self-employment income, which reduces self-employment tax on top of the federal deduction benefit.

Bottom Line

If you own any part of a business in a high-tax state and your tax professional has not brought up the PTET election, ask them about it! It must be elected annually, and the deadlines vary state by state. For high earners running an S-corp, partnership, or multi-member LLC, or anyone collecting a K-1, it is one of the most powerful tools in your tax planning arsenal.

Frequently Asked Questions

How do I know if PTET is worth it for my business?

PTET tends to be most valuable when your pass-through income is substantial enough that your state tax bill exceeds the federal SALT cap, which is $40,400 for 2026. If you own an S-corp, partnership, or multi-member LLC in a high-tax state like California, New York, New Jersey, or Hawaii and your business generates significant income, there is a good chance PTET saves you money. The calculation depends on your specific income level, state tax rate, ownership structure, and whether your personal itemized deductions already exceed the standard deduction. The best next step is to ask your CPA to model the election for your 2026 return before your state's deadline passes.

Wondering if a PTET election could lower your tax bill?

Book a free intro call. We'll look at your business structure, your state's rules, and how PTET fits your overall financial plan.